Notifications

Copies of public submissions made to the Board are available below. Where an Islamic financial product is economically equivalent to a conventional product, the tax treatment of the two products should be the same. We hold a restricted ADI authorisation granted by the Australian Prudential Regulation Authority .

Second, the Report called for an inquiry by the Board of Taxation into whether Australian tax law needs to be amended to ensure that Islamic financial products have parity of treatment with conventional products. This will give new financing opportunities to Australian businesses looking to start up or expand. It will also support the availability of infrastructure financing because it is well suited to longer-term and large projects. This will provide a level playing field for equivalent asset backed and conventional financing arrangements and will enable Australian businesses to more easily access investment at more competitive rates.

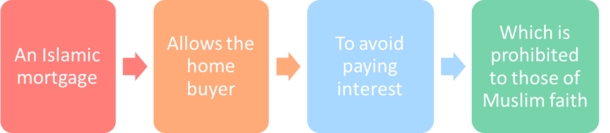

To meet with Islamic law requirements, finance needs to be structured as a lease where rent and service fees are paid instead of interest or some other kind of profit-sharing arrangement. Moreover, before you apply for a specific loan, please make sure that you’ve read the relevant T&Cs or PDS of the loan products. You can also check the eligibility requirements to determine whether the product is right for you or not. Although, technically, interest isn’t charged for an Islamic home loan, the financial institution will still be charging fees in the form of rent or profit rate.

Islamic home loans are available for many purposes such as construction and purchasing vacant land, Sharia Home Loans Australia although they are not typically used for refinancing. They also come in full documentation and low documentation versions, depending on your leasing needs. Speaking to The Adviser on the occasion of the RADI being granted, Islamic Bank Australia chief executive Dean Gillespie outlined that the bank will look to distribute home finance through the broker channel, as well as direct. Settle Easy has updated its online platform to provide automatic updates to mortgage brokers and real estate agents during the conveyancing ...

Without this approach, the gap on financial inclusion will only widen or contribute to diminishing financial health. When I spoke at the Islamic finance symposium just 11 months ago, it was hard to imagine the growth in interest from all sides in this global phenomenon. Geographically, Australia is well positioned within the Asia Pacific region to expand already strong trade linkages with the region through the Islamic finance sector.

"The question for them arose whether they could actually undertake the Islamic banking activities within the Australian framework. And the decision was made that that was quite a difficult prospect." Some time ago, Amanah Finance's Asad Ansari consulted for an offshore Islamic bank that was interested in setting up a branch in Australia. Imran says NAB isn't looking to play in the consumer Islamic finance space. He believes the big opportunity for Australia is setting up mechanisms that can allow offshore companies to invest here. "I'm a Halal butcher, with a Halal investment, and a Halal superannuation."

We’re working as fast as we can to achieve our full ADI licence and bring our products to the Islamic community and all Australians,” Mr Gillespie said. The report concluded Australia has arguably the most efficient and competitive financial sector in the Asia-Pacific region, but there are further opportunities to expand our exports and imports of financial services. Australia is highly regarded internationally as a place to do business.

Saving People from Riba

Over time, the client pays off the house through rental payments, which include a profit to the financier and reflect market interest rates. Eventually, the asset is wholly paid off by the client and they own the house outright. Fees and charges may apply, as well as terms and conditions which you should review. In order to open a credit product in future, you will need to meet our credit criteria and be approved. Please review the product disclosure documentation provided at the time of opening your account for detailed information.

There is still a lack of information about financial exclusion according to ethnicity or religious group in Australia. The Muslims communities are financial excluded mainly due to their faith and religious beliefs, because Islam prohibits Riba which is widely practiced in conventional banking and finance operations. The level of awareness about the Islamic finance products and services in Australia is still limited. Also the lack of Islamic financial products and services is a contributory factor of financial exclusion. The introduction and wide spread offer of Shariah-compliant financial products and services by Islamic and conventional financial institutions can increase nationwide financial inclusion. Some argue that Islamic finance simply interchanges terminology and concepts and that Sharia-compliant home loans don’t differ greatly from standard home loans.

Having recently received our restricted banking licence, this role is part of a small team bringing new banking products to the Australian market. Gus is passionate about developing, designing and implementing digital products and services to help businesses across Australia accelerate innovation at the pace of customer expectations. However, with technology rapidly evolving, banks and financial institutions are challenged with having to innovate at the pace of the customer — and perhaps even more difficult, their expectations for delightful experiences. Islamic Finance Such restrictions not only impact the bottom line of banks and financial service providers, but so too, do they have a negative impact on the quality of life for Australian Muslims. It could be argued that the latter is more important to creating a thriving, inclusive society and has a bigger impact on the economy in the long term. Providing or obtaining an estimated insurance quote through us does not guarantee you can get the insurance.

Instead, they follow Mudarabah principles and earn you money through profit shares. There’ll be term deposits available from 1 to 12 months, and an automated rollover feature that puts your money back in a term deposit when it hits its maturity date. Sharia Law offers Muslims a broad set of rules for living an ethical life.

But after the couple married in 2018, they started using an Islamic financing company to buy property. They've now flipped three houses, all using the same financier. With roughly 600,000 people identifying as Muslim in Australia, industry Halal Finance reports place the potential size of this market in Australia at $250 billion. We are a Restricted ADI and do not yet meet the full prudential framework, and you should consider this before banking with us once we are open for business. Information on this website does not take your personal circumstances, needs or objectives into account.

Islamic Home Loans Compare Islamic Home Loan Options

We are rigorous about ensuring the Shariah integrity of our products through Shariah audits and on-going testing. We pride ourselves in engaging with a range of local Islamic scholars and we are the only provider to be endorsed by the Board of Imams Victoria and President of the Imams Council of Queensland . Invest your funds in our Investment Islamic Bank In Australia Grade Income Fund with quarterly predictable returns. Getting home finance can seem complex, even if you’ve bought property before. The difference between the two scenarios from a Shariah point of view is that the 20% made from selling the car is a permissible profit , while the 20% interest on a loan is the pure definition of prohibited Riba .

Consider whether this advice is right for you, having regard to your own objectives, financial situation and needs. You may need financial advice from a suitably qualified adviser. For more information, read Canstar’s Financial Services and Credit Guide and our detailed disclosure. Canstar may receive a fee for referring you to a product provider – for further information, see how we get paid. Various forms of Islamic home financing are offered by a handful of service providers in Australia. This combination of rental and sale contract makes it the best halal financing product for property ownership while you get to own the house of your dreams and call it home.

InfoChoice lists more than 2,000 financial products from 145 Australian banks, credit unions, building societies and non-bank lenders. With a conventional, non-Sharia mortgage, you’d buy the property with a mortgage agreement that involves funds borrowed from the lender. You’d then repay the loan, with interest, over a set repayment period. Islamic finance is based on a belief that money should not have any value itself, with transactions within an Islamic banking system needing to be compliant with shariah . Sharia – compliant loans take roughly the same time to arrange as western-style mortgages. That can involve valuations and a detailed examination of your personal financial circumstances so it’s a good idea to allow a few weeks.

![]()

There is a Islamic Home Finance Australia misconception amongst the general public that Islamic finance is the same as conventional, simply because both specify the finance cost as a percentage. This is a huge misnomer because using a percentage is just a method of pricing. Hence, what is most important is not the use of the percentage, but rather what such a percentage represents.

The bank hopes to obtain APRA approval to offer its products to the general public by 2024. Initially, Islamic Bank Australia will offer everyday accounts, term deposits and home loans. The Islamic Bank Australia will offer banking services